The Gulf Cooperation Council is in the middle of one of the most consequential financial-services transformation cycles in its history. Saudi Arabia’s Vision 2030, the UAE’s digital-economy strategy, Bahrain’s fintech-hub ambitions, Kuwait’s transformation programme and Qatar’s financial-centre development. All together have created the most ambitious, best-funded and fastest-executing modernisation agenda in the emerging world. And underneath all of it sits a single, unglamorous question.

This guide takes that question, and the ones that follow from it, in the order a banking or fintech leader in the region would actually ask them. The answers determine which institutions lead the GCC market of 2028 and which are still constrained by systems built for a different era.

The GCC opportunity, in three numbers

| >$4T Combined banking assets across the six GCC member states | ~50% Of all global Islamic finance assets sit in the GCC | 15+ yrs Average age of incumbent GCC core banking systems |

Sources: GCC central-bank data; Coalition Greenwich; IFSB.

The Question Beneath Everything

Every Gulf institution has a digital strategy. So what is the real constraint on executing it?

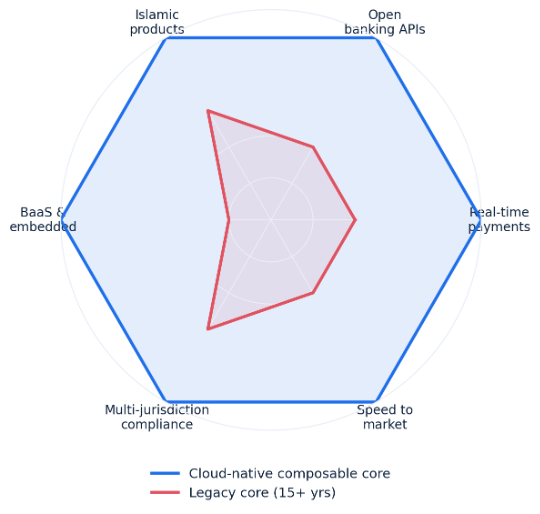

The core. Behind the polished apps and biometric logins, the decisive battle is being fought in the back office. The average core banking system in a GCC incumbent is more than fifteen years old, built for branch-based banking, batch processing and a largely static product set. These systems were never designed for real-time payments, open-banking APIs, Islamic BNPL, embedded finance or the Banking-as-a-Service partnerships the Gulf’s digital economy now demands.

This is the defining gap in the region: the distance between what institutions want to launch and what their infrastructure can actually support. Closing it with cloud-native, composable core banking technology is, in plain terms, the highest-leverage technology investment available to a GCC institution in 2026.

Figure 1. Capability gap. A legacy core can be patched at the edges, but the structural distance from a cloud-native, composable platform is widest precisely where the GCC market is growing fastest.

The Scale of the Prize

Is the GCC really large enough to justify purpose-built investment?

Comfortably. Combined banking assets across the six member states exceed four trillion dollars. The region holds among the world’s highest concentrations of wealth, one of the youngest demographic profiles of any high-income bloc, and some of the highest smartphone-penetration rates anywhere. Formal financial-services penetration is already high by emerging-market standards and is climbing as digital channels strip out friction.

The regulators are not bystanders. SAMA’s fintech accelerator in Saudi Arabia, the CBUAE’s regulatory sandbox in the UAE and Bahrain’s digital-banking framework have each built structured pathways for new entrants. The number of licensed fintechs across the GCC has gone from a handful in 2018 to several hundred in 2026, with the application pipeline still growing.

What the Market Requires

We keep hearing Islamic banking is “nice to have.” In the Gulf, is that true?

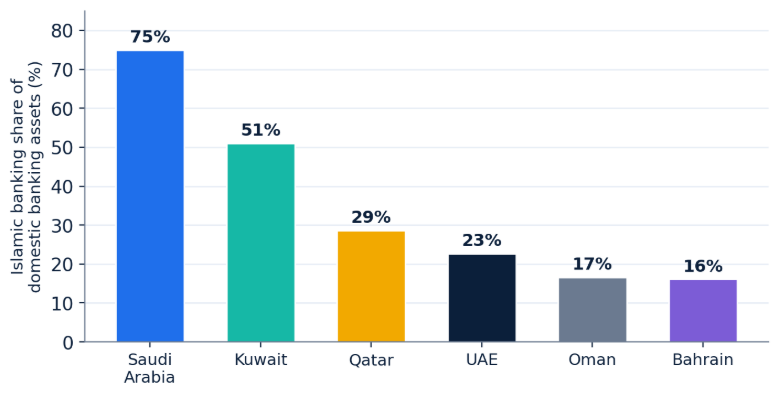

No. In the GCC it is a condition of entry, not a differentiator. The region is the global heartland of Islamic finance: roughly half of all global Islamic-finance assets sit here. Saudi Arabia is Islamic by regulatory design, with every bank in the Kingdom required to comply with Sharia principles; Islamic banking already accounts for around three-quarters of domestic banking assets there. The UAE runs both models with a fast-growing Islamic share, Bahrain hosts the sector’s two main standard-setters in AAOIFI and IFSB, and Qatar and Kuwait carry substantial Islamic sectors of their own.

Figure 2. Islamic banking as a share of domestic banking assets. Across the Gulf, Sharia-compliant capability is not a niche; in Saudi Arabia and Kuwait it is the majority of the market.

A platform serving these markets must therefore treat the full range of Islamic structures, Murabaha, Ijara, Diminishing Musharaka, Mudaraba and Wakala, as native, first-class product types: with the right data models, AAOIFI-aligned accounting treatments, Sharia audit trails and Sharia-board interface capabilities. Bolting Sharia compliance onto a conventional core after the fact does not meet this bar.

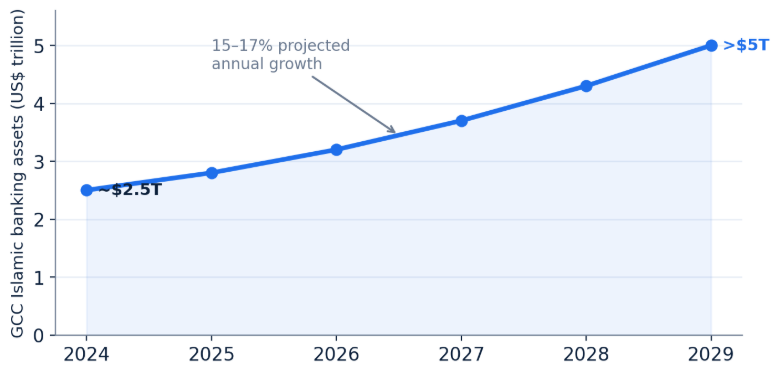

The growth case reinforces the point. GCC Islamic banking assets, around $2.5tn in 2024, are projected to exceed $5tn by 2029, expanding at roughly 15–17% a year.

Figure 3. GCC Islamic banking assets, projected trajectory. Indicative, based on Coalition Greenwich and industry estimates.

Multi-jurisdiction compliance

The GCC is not one regulatory jurisdiction but six. SAMA, the CBUAE, the CBB in Bahrain, the CBK in Kuwait, the QCB in Qatar and the CBO in Oman each maintain distinct frameworks, reporting requirements and product-approval processes. A platform genuinely built for the Gulf has to generate compliant reports for each, implement each central bank’s specific product rules, and hold the data structures each framework needs. For groups operating across several markets, it must also handle consolidated reporting, inter-entity transfer pricing and regulatory capital across multiple licensed entities.

Regional payment-network integration

Each member state runs its own national payment rails, and the region is now stitching them together through the Arab Regional Switch and bilateral links. A credible GCC platform needs pre-built, production-proven integration across the systems that move money in the region:

- SARIE (Saudi Arabian Riyal Interbank Express) for domestic real-time payments in the Kingdom.

- IPP and UAEFTS for instant and funds-transfer payments inside the UAE.

- SWIFT for international cross-border payments and trade-finance messaging.

- GCC Card Scheme for domestic card transactions.

- Wage Protection System (WPS) for the payroll-compliance obligations that are mandatory in the UAE and Saudi Arabia.

Localisation and data sovereignty

Localisation in the Gulf goes well past translation. Arabic has to work as a primary language for customer documents, statements and communications; the Hijri calendar is required for Islamic contract documentation and parts of regulatory reporting; and Arabic name formats, address structures and national ID types such as the Emirates ID, the Iqama and the Saudi National ID have to live natively in the customer data model.

Sovereignty is non-negotiable. Both the CBUAE and SAMA require customer financial data to be processed and stored within their own jurisdictions. A cloud-native platform must therefore be deployable so that all processing happens inside UAE or Saudi cloud regions. Fimple’s architecture supports in-country deployment through the major cloud providers’ UAE and Saudi availability zones.

Where Fimple Sits

Plenty of vendors claim the GCC. What makes a regional presence real rather than a sales office?

Fimple has operated in GCC markets since it was founded in 2022, with offices in Dubai and Riyadh. The point worth stressing is what that presence is for. It is not a sales-and-marketing footprint; it is a product-development, regulatory-engagement and customer-success operation. The GCC team includes regulatory-compliance specialists who work directly with the CBUAE, SAMA and other central banks on product approvals, reporting requirements and sandbox participation, which keeps the platform’s regulatory capabilities current as the rules evolve.

On the ground, the client base spans both sides of the market. Financial-institution clients deploy Fimple’s core banking, Islamic banking, trade-finance and BaaS capabilities. Non-financial enterprises use the BaaS-ready platform to launch embedded products, BNPL, savings accounts and payment solutions, inside their existing customer relationships.

The Quiet Giant: Non-Financial Institutions

Where is the demand the rest of the market is underestimating?

In companies that are not banks. One of the distinctive features of the Gulf’s digital economy is the scale and sophistication of non-financial players now adding financial services to what they already do, which creates a large and fast-growing market for BaaS infrastructure.

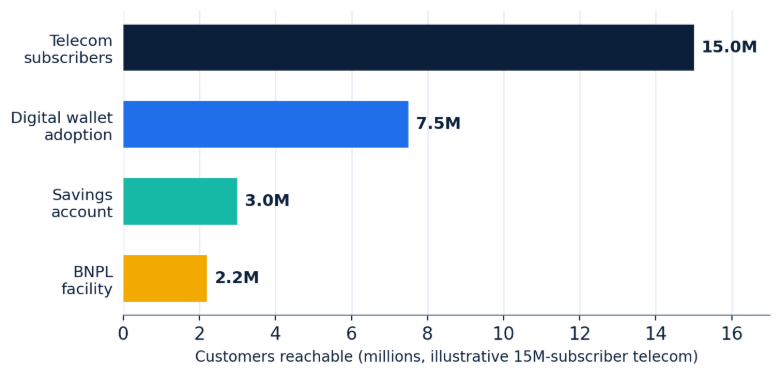

Telecoms are the clearest illustration. Several GCC operators rank among the world’s largest by subscriber count. A telecom with fifteen million subscribers that can offer each of them a wallet, a savings account and a BNPL facility becomes a financial-services business at scale without ever holding a banking licence, provided the BaaS platform underneath is built on composable core banking. The figure below shows how even conservative adoption rates turn a subscriber base into millions of financial-product relationships.

Figure 4. The embedded-finance funnel for a single 15-million-subscriber telecom. Illustrative adoption rates; the point is the order of magnitude.

E-commerce and retail platforms are following the same logic, embedding BNPL, merchant financing and seller-payment solutions to deepen both buyer and seller relationships. And government entities are increasingly building payment of fees, instalment options for public services and identity-linked accounts directly into digital-government platforms, another BaaS use case being explored across the bloc.

Why the Decision Is a 2026 Decision

The case is clear. But why move now rather than in two years?

Because the market is at an inflection point and the window is open but narrowing. The first wave of cloud-native adoptions, by digital banks and fintechs, has already proven the model. Incumbents are now accelerating their own modernisation. As pressure from digital challengers becomes impossible to ignore, and non-financial institutions are building financial-services capability at scale.

The arithmetic of delay is unforgiving. Institutions that commit to cloud-native technology in 2026 will be shipping products and partnerships in 2027 and 2028. That legacy-constrained competitors simply cannot replicate. Those that wait will watch the gap between their capabilities and the market standard widen with every quarter.

What This Means in Practice

For a leader weighing the decision, the GCC requirements reduce to a short, demanding checklist. That a credible platform must satisfy on day one:

- Islamic-native, not Islamic-retrofitted. Sharia structures as first-class products with AAOIFI-aligned accounting and audit trails.

- Six jurisdictions, one platform. Compliant reporting and product rules for each GCC central bank, plus cross-border group management.

- Wired into regional rails. Production-proven SARIE, IPP/UAEFTS, SWIFT, GCC Card Scheme and WPS integration.

- Sovereign by design. In-country deployment within UAE and Saudi cloud regions, with full Arabic and Hijri support.

- BaaS-ready for the non-bank wave. Composable infrastructure that lets telecoms, retailers and governments embed finance at scale.