A practitioner’s field guide to where artificial intelligence is delivering measurable ROI today, across credit, fraud, compliance, customer experience and operations, and what GCC, African and CIS institutions need in place to capture it.

Artificial intelligence in banking has quietly crossed a threshold. It is no longer a line item in an innovation budget or a slide in a strategy offsite. It is running in production. In 2026, models approve loans in under a second, surface fraud rings that no rule could describe, draft regulatory filings that once consumed teams of analysts, and answer customers in natural language with live account context. The interesting question is no longer whether AI works in banking. It is why some institutions extract compounding value from it while others remain stuck in perpetual pilots.

This guide is deliberately practical. Rather than survey the field in the abstract, it walks through the questions banking leaders in our markets actually ask, and answers each with the specific use cases, economics and architectural prerequisites that determine success. The structure is a conversation, because that is how these decisions really get made.

The stakes, in three numbers

| ~$2T Estimated annual value AI could add to global banking | 2.84x Return multiple for AI frontrunners vs. 0.84x for laggards | 45% Of bank AI initiatives never reach production |

First Principles

Before we talk use cases, what actually determines how much value a bank can get from AI?

Its core. This is the unglamorous answer, and the most important one. An AI model is only ever as good as the data it can reach, the speed at which it reaches it, and the reliability with which it can act on the result. A cloud-native, API-first, real-time core records every transaction immediately in structured form, publishes every event to a stream a model can subscribe to, and exposes every banking function through a documented API. A batch-processing legacy core offers data that is hours or days old, locked in formats that require heavy engineering before a model can touch it, with no clean way to act in real time.

The implication is strategic rather than technical: investment in a modern core is also investment in AI readiness. Institutions that have already modernised find that each new AI capability arrives faster and cheaper than it does for competitors still wrestling with legacy systems. This is also why fragmented AI fails to scale: when every use case is built on a different data model with its own integration path, the combined overhead eventually exceeds the savings of any single initiative.

Use Case 1: Credit Decisioning & Underwriting

Our bureau data is thin. Can AI really lend to customers we currently can’t score?

Yes, and for our markets this is arguably the single most consequential application. Traditional decisioning leans on a handful of inputs: a bureau score, income verification, employment status, and a loan officer’s judgement for anything that doesn’t fit the template. That approach structurally excludes the credit-invisible, customers without a bureau history, and tends to be slower and less accurate than machine learning for many segments.

Machine-learning models, by contrast, can weigh hundreds of variables drawn from dozens of sources: transaction patterns, repayment behaviour on existing products, consented telco usage, e-commerce history, seasonal income variation, and more. In Egypt, Saudi Arabia and much of sub-Saharan Africa, where a large share of the population has no bureau file or a thin one, models trained on alternative data can extend credit to these segments in a way that is both commercially viable and financially inclusive, growing the book while keeping risk manageable.

A note on Islamic finance. For Islamic BNPL and other Shariah-compliant products, the decision is reframed: not “should we lend at this rate?” but “should we sell this asset on deferred terms at this markup?” The risk assessment rhymes with conventional underwriting, but the product structure, accounting treatment and regulatory framing differ, so models must be trained on the specific structures they will support, not retrofitted from a conventional lending model.

Reported impact is concrete: McKinsey documents a US bank that rebuilt its credit-risk memo process with AI agents and saw a 20–60% productivity gain and roughly 30% faster turnaround. Standard applications that took 48 hours increasingly resolve in real time.

Use Case 2: Real-Time Fraud & Financial Crime

Our rules engine drowns analysts in false positives. What changes with AI?

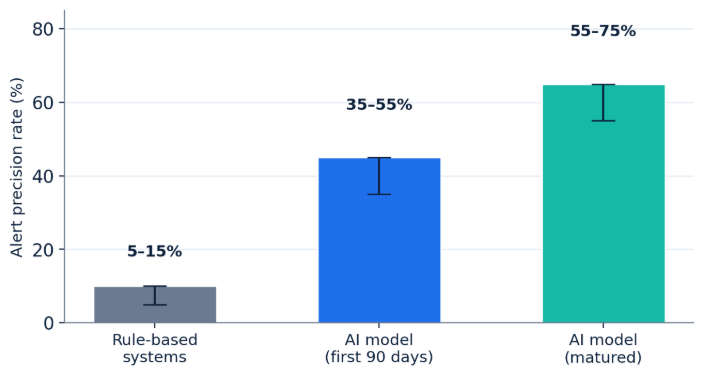

The economics change. Rule-based systems force a painful trade-off: tighten the rules and you decline legitimate customers; loosen them and you miss sophisticated fraud that never matched a rule in the first place. Most rule engines run at 5–15% alert precision, meaning the overwhelming majority of alerts are noise that analysts must still clear by hand.

Machine-learning models learn each customer’s normal behaviour and flag meaningful deviations: an unusual foreign-currency request at an odd hour, a sequence of small transfers matching a structuring pattern, a spike in activity after dormancy. Crucially, they adapt. Fraudsters constantly evolve; a rules system needs manual updates to keep pace and is therefore always a step behind, while a model can be retrained on recent fraud to catch new patterns before anyone has written them down. Well-calibrated models reach 35–55% precision within the first 90 days and keep improving as analysts feed back outcomes.

Figure 1. Alert precision: the share of fraud alerts that prove to be real. AI models start meaningfully higher than rule engines and compound from there.

Graph analytics for AML. Traditional monitoring inspects each customer’s transactions in isolation. Graph neural networks instead read the network of relationships between accounts: who moves money to whom, how often, through which chains. Laundering structures built from rings of accounts designed to break large sums below reporting thresholds are visible to graph analysis in ways single-account monitoring simply cannot see. For UAE and Saudi banks clearing high volumes of international transfers, this is a step-change in detection and a real reduction in manual suspicious-activity review.

Context for the board: Juniper Research estimates AI-based fraud prevention saved the global banking sector roughly US$10.4bn in 2025, while leading deployments report up to a 60% cut in false positives.

Use Case 3: Intelligent Regulatory Compliance

Compliance is our largest manual cost centre. Where does AI actually bite?

In two places. The first is regulatory reporting. Banks in GCC markets file hundreds of reports a year (liquidity, capital adequacy, large-exposure notifications, suspicious-activity reports, consumer-finance disclosures), each requiring data to be extracted, transformed, validated and submitted on a deadline. AI now automates this end to end: extraction models pull the required fields regardless of how they are stored, validation models check internal consistency and flag anomalies before submission, and natural-language models monitor regulators’ own publications, flagging changes that demand a new report format or process.

The second is dynamic transaction monitoring. Rather than waiting for compliance teams to hand-update detection rules, AI-assisted monitoring learns from the outcomes of manual review, seeing which alerts became filings and which were dismissed, and adjusts sensitivity to lift the signal-to-noise ratio over time.

One caution worth stating plainly: in regulated domains, governance is not a brake on AI; it is the mechanism that makes adoption possible. Every model that influences credit, fraud or compliance outcomes must be explainable, auditable and continuously monitored. The EU AI Act already classifies credit scoring as “high-risk,” and regional regulators are moving the same way. Treating explainability as living infrastructure rather than after-the-fact documentation is precisely what lets the fast movers move fast.

Benchmark: Deutsche Bank’s reporting-automation programme is reported to have cut MiFID II compliance costs by roughly €47m a year while improving reporting accuracy by around 85%.

Use Case 4: Intelligent Customer Experience

Aren’t AI assistants just the old chatbots with better marketing?

Not anymore. The scripted decision-tree bots of the last decade and today’s LLM-powered assistants are different species. A modern banking assistant understands a genuinely complex question, pulls live account data through core APIs, walks a customer through a multi-step journey such as a product application or dispute, and hands off to a human with full context when judgement is required. Industry data suggests 40–60% of inquiries can now be resolved without human escalation.

Personalisation at scale. The same real-time data lets a bank tailor offers, pricing and messaging at the level of the individual customer. A retail bank can extend a savings-rate incentive precisely to customers whose transaction patterns suggest they are about to move deposits elsewhere; a corporate bank can surface a trade-finance facility at the exact point in a client’s operating cycle when working-capital need peaks. This is where customer experience quietly becomes a revenue and retention engine rather than a cost centre.

Use Case 5: Operations Intelligence & Automation

Where are the fastest, least glamorous wins hiding?

In the back office. Trade finance is the clearest example. Letters of credit, bills of lading, insurance certificates, inspection reports and invoices all have to be checked against LC terms, work that historically demanded experienced specialists poring over scanned documents. AI document-intelligence models extract and validate this data at accuracy matching or exceeding manual teams. At a fraction of the time and cost. For UAE banks in particular, given the country’s role as a global re-export hub. This turns a multi-day process into hours and delivers immediate, measurable savings.

Predictive operational risk. Models watching core-system telemetry such as latency, error rates and throughput can predict infrastructure problems before they cause an outage. Shifting the operation from reactive firefighting to proactive maintenance and shrinking the customer impact of incidents from hours to minutes.

McKinsey’s work on agentic AI in service operations estimates a 30–50% reduction in manual workloads once agents are deployed at scale.

Sequencing the Investment

If we can’t do everything at once, what should we deploy first?

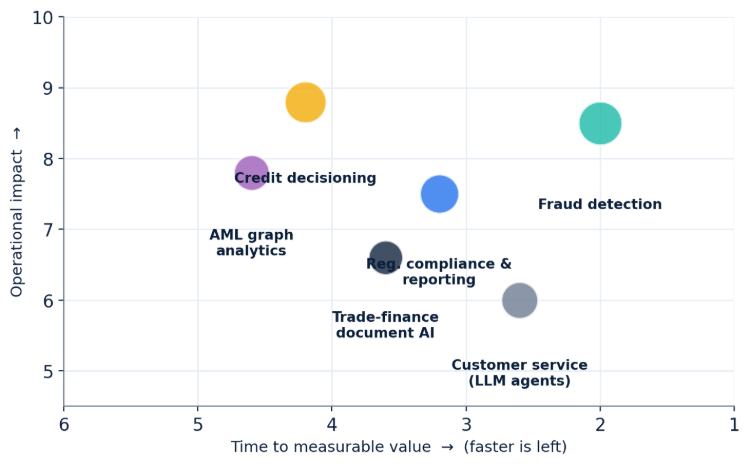

Lead with the decision layer. Fraud, AML, credit and compliance, especially in “shadow mode”. Where the model runs alongside existing systems without taking action, deliver quick, low-risk, measurable gains while satisfying model-risk management. Progress comes from what practitioners call tractable wedges: small, contained deployments that prove value and then scale safely. The figure below maps the major use cases by speed-to-value against operational impact.

Figure 2. Where AI lands first. Fraud detection and compliance reporting reach measurable value fastest. Credit decisioning and AML graph analytics carry the highest impact once matured.

The size of the prize

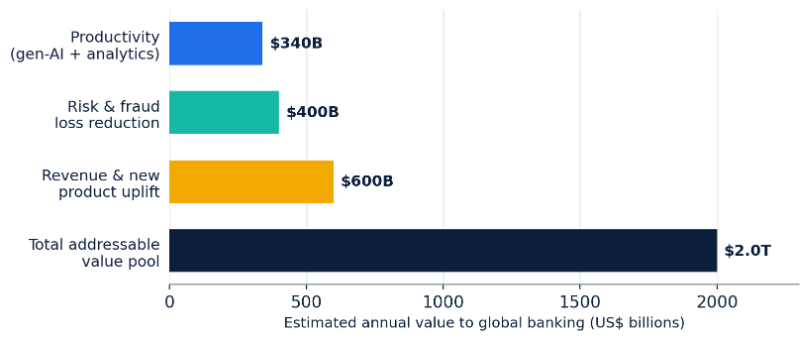

McKinsey’s 2025 Global Banking Annual Review estimated that generative AI and advanced analytics could add US$200–340bn in annual value to global banking through productivity alone. Once revenue generation, risk reduction and new products are included, the identified, quantifiable opportunity expands to roughly US$2tn a year.

Figure 3. Illustrative aggregation of AI value pools in global banking. Figures are indicative and drawn from the sources listed.

Why Early Movers Pull Away

Is there really a first-mover advantage, or is that just vendor talk?

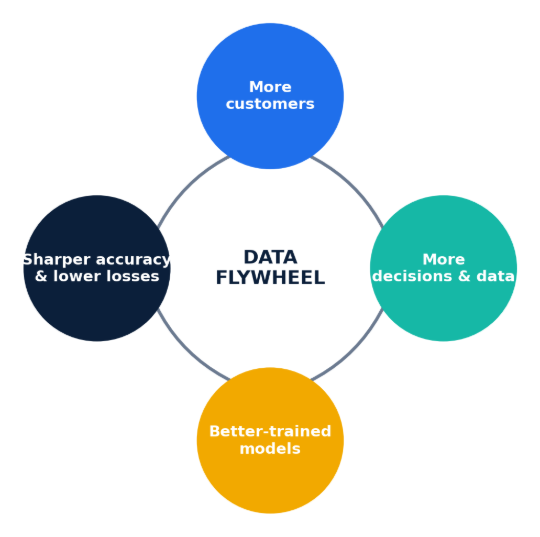

There is, and it compounds, because of the data flywheel. A model improves as it sees more data. A credit model that makes a million decisions learns more than one that makes ten thousand. A fraud model watching a billion transactions sees patterns one watching a million never will. The institution that deploys today accumulates decision data that sharpens next year’s models. The one that waits starts with less data and weaker models, and the gap widens each year.

Figure 4. The data flywheel. Each turn produces data that improves the next, creating a compounding, not linear, advantage.

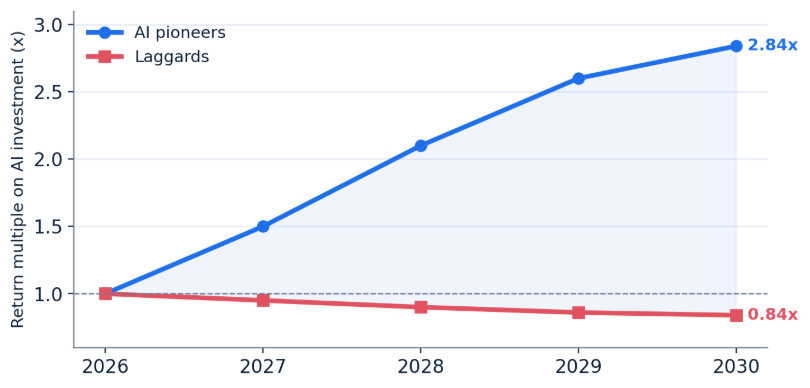

In markets where credit data is scarce. As it is across much of the African and GCC addressable base, this advantage is even more pronounced, because early adopters are effectively building a proprietary data asset that latecomers cannot simply buy. The market-level evidence is already visible: research places AI frontrunners at a 2.84x return on investment against just 0.84x for laggards.

Figure 5. The divergence. Pioneers compound returns while laggards fall below break-even; the gap, once open, is hard to close. (Indicative, based on IDC and McKinsey findings.)

What This Means in Practice

If there is a single thread running through all five use cases, it is that the model is rarely the hard part. The hard part, and the durable advantage, is the foundation underneath it:

- Modern core first. Real-time, API-first data is the prerequisite for every use case above; legacy batch cores cap what AI can ever achieve.

- Start in the decision layer. Fraud, AML and compliance offer the fastest, lowest-risk, most measurable returns, ideally in shadow mode first.

- Govern from day one. Explainability and auditability are what let regulated institutions deploy quickly rather than slowly.

- Build the flywheel early. In data-scarce markets, the proprietary data accumulated by moving first becomes a moat competitors cannot purchase.

- Treat AI as horizontal infrastructure, not a portfolio of disconnected pilots. Fragmentation is the most common reason value never scales.